IR35 Calculator 2026/27: Inside vs Outside IR35 Take-Home Pay Comparison

If you’re a UK contractor evaluating a new contract, the IR35 Calculator for 2026/27 is essential. A £500/day rate can look attractive until you compare inside vs outside IR35 take-home pay. IR35 (off-payroll working rules) can reduce your net earnings by 20-30% or more if you’re deemed inside. Use this guide and the IR35 Calculator insights below to run accurate numbers before signing.

Contractor Details

Enter your day rate and working days to compare IR35 scenarios

- Outside IR35: salary at personal allowance (£12,570), remaining profit taken as dividends

- Corporation tax at 19% (small companies rate)

- Dividend allowance: £500

- Inside IR35: full revenue flows through PAYE

(5.3% of revenue)

Email me my results

Get insider updates on IR35 comparison — plus the 5-year cost of getting it wrong at £500/day — emailed instantly.

For accountants and bookkeepers

Your clients are asking this question every week. Put this calculator on your site so they get the answer themselves, then get notified when they’re ready to act.

See how the widget works →What is IR35?

IR35, or the off-payroll working rules, targets “disguised employees” — contractors working like permanent staff but paid via a limited company (PSC). If your engagement falls inside IR35, the client or fee-payer deducts PAYE tax and National Insurance (NI) at source, treating income as employment earnings. This IR35 Calculator guide helps you quantify the impact.

Inside vs Outside IR35: Key Differences

| Aspect | Outside IR35 | Inside IR35 |

|---|---|---|

| Payment Structure | Small salary + dividends | Deemed employment (PAYE on invoice value) |

| Tax Applied | Corporation tax + dividend tax | PAYE income tax + Employee/Employer NI |

| Business Expenses | Fully claimable | Limited (no 5% allowance in Chapter 10) |

| Tax Efficiency | High (dividend optimisation) | Low |

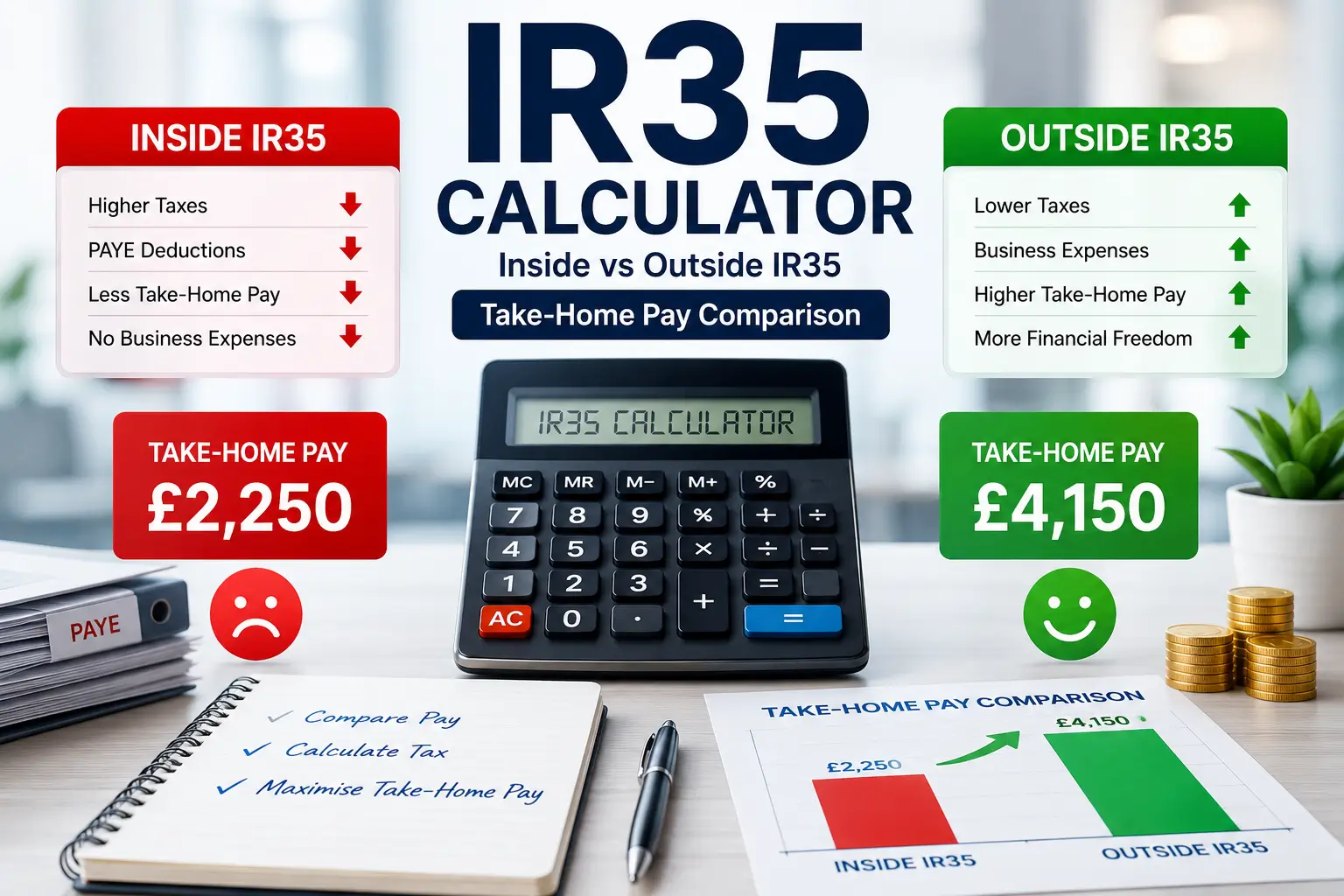

| Take-Home Impact | Typically 70-80% retention | 55-65% retention (20-30% less) |

Outside IR35 lets you operate as a genuine business. Inside IR35 removes most tax planning, with full employer NI (15% in 2026/27) often absorbed into the rate.

Worked Example: £500/Day Contract (IR35 Calculator 2026/27)

For a £500/day rate over 220 days (£110,000 annual gross):

- Outside IR35 (Ltd Co, optimal salary + dividends): After corporation tax (19-25% with marginal relief), £12,570 salary, and dividend tax (10.75%/35.75% above £500 allowance), take-home is typically £68,000–£72,000+ (depending on expenses/pension). Effective rate ~35-38%.

- Inside IR35: Employer NI (15%) deducted first, then PAYE + employee NI. Take-home often £55,000–£62,000 — roughly 20-30% lower.

Run your exact figures in a dedicated IR35 Calculator for precision, factoring expenses, pensions, and location.

Day Rate Equivalent Inside IR35

To match outside IR35 take-home, an inside IR35 day rate often needs a 10-30% uplift (exact % varies by rate, expenses, and tax bands). For a £500/day outside rate, you might need £545–£650+ inside to break even. Always use an IR35 Calculator 2026/27 rather than rough estimates.

How Much Less Do I Take Home Inside IR35?

Most contractors lose 20-30% take-home on the same day rate inside IR35 due to:

- Full 15% employer NI deducted upfront.

- PAYE income tax + 8%/2% employee NI.

- No dividend optimisation or full expense relief (especially Chapter 10).

- Lost 5% flat-rate allowance in many cases.

IR35 Calculator results consistently show £10k–£18k+ annual difference on £100k–£120k contracts.

Key IR35 Status Factors

HMRC assesses overall picture (not one factor):

- Control (how/when/where you work).

- Substitution (genuine right to send a replacement).

- Mutuality of Obligation (ongoing work guarantee).

- Financial Risk (investment, cost overruns).

- Integration (treated like staff?).

Document everything for your IR35 Calculator status defence.

Using HMRC’s CEST Tool

CEST (Check Employment Status for Tax) provides a useful indication. An “outside” result generally protects you if answered honestly. Combine with professional review for complex roles.

Who Determines IR35 Status?

- Medium/Large Clients & Public Sector: Client issues Status Determination Statement (SDS).

- Small Private Companies (turnover ≤£15m, balance sheet ≤£7.5m, or <50 employees from April 2026): Contractor’s PSC decides.

How to Challenge a Status Determination

Submit written evidence within the process. Client has 45 days to respond. Failure to reply or blanket approach can shift liability. Keep records of working practices.

Blanket Determinations

Generic “inside” rulings without individual assessment often fail “reasonable care.” Strong grounds for challenge.

The IR35 Offset — Avoiding Double Taxation

Since April 2024, tax already paid (income tax, dividends, corp tax, employee NI) offsets against deemed employer liability. Employer NI remains extra.

5% Expenses Allowance: Chapter 8 vs Chapter 10

- Chapter 8 (small clients, self-assessed): 5% flat allowance for admin costs.

- Chapter 10 (medium/large): No allowance — actual expenses only (limited).

2026/27 Tax Rates You’ll Need for IR35 Calculator

- Personal Allowance: £12,570

- Income Tax (England etc.): 20% basic (£12,571–£50,270), 40% higher, 45% additional.

- Employee NI: 8% (£242–£967/week), 2% above.

- Employer NI: 15% above £96/week secondary threshold.

- Dividend Allowance: £500; rates 10.75% basic, 35.75% higher, 39.35% additional.

- Corporation Tax: 19% (≤£50k), marginal relief to 25% (>£250k).

Scotland: Separate bands (e.g., higher 42%, advanced 45%, top 48%). Use location-specific IR35 Calculator.

Umbrella Company Fees

£15–£30+/week typical. Compare providers, especially with new JSL risks.

Pension Contributions and Take-Home Pay

Salary sacrifice or employer contributions boost nets significantly (especially inside). Plan around future NI on higher sacrifices (from 2029).

Joint & Several Liability Rules (April 2026)

New rules make agencies (or clients) jointly liable with umbrellas for unpaid PAYE/NI — no safe harbour from due diligence. Increases risk of umbrella route; many shift toward outside IR35 or SoW models.

HMRC Investigation Risks and Penalties

Penalties 30-100%+ of tax owed for careless/deliberate errors. Strong documentation and IR35 Calculator modelling reduce risk.

IR35 Insurance

Covers enquiry costs and representation — valuable protection.

Industry-Specific Notes

IT/tech most scrutinised. Finance and healthcare often see more inside determinations due to control/integration.

Employer Perspective: IR35 and Off-Payroll Compliance

Clients must issue SDS, operate PAYE if inside, and respond to challenges. Factor extra employer NI costs.

FAQs on IR35 Calculator 2026/27

What is IR35?

IR35 (also called the off-payroll working rules) is UK legislation that determines whether a contractor working through a limited company should be taxed as an employee.

What is the difference between inside and outside IR35?

Outside IR35, you run a genuine business — small salary plus dividends, paying corporation tax and dividend tax. Inside IR35, the engager applies PAYE tax and NI directly to your invoice income, with no dividend tax efficiency.

How much less do I take home inside IR35?

Typically 20–30% less for the same day rate, mainly due to full employer NI, employee NI, and income tax being applied with no dividend tax optimisation.

Who determines IR35 status?

For public sector and medium/large private clients, the client determines status via an SDS. For small private companies, the contractor’s own limited company remains responsible.

What are the key IR35 status factors?

Substitution, Control, and Mutuality of Obligation are the three main pillars, alongside Financial Risk and Integration.

Can I challenge an IR35 status determination?

Yes, through the client-led disagreement process. The client has 45 days to respond, and the original status applies during that time.

What is the IR35 offset?

A mechanism (since April 2024) that lets HMRC offset tax you’ve already paid against what a deemed employer owes, to avoid double taxation.

What is joint and several liability (JSL)?

From April 2026, HMRC can recover unpaid PAYE/NI from an agency or end client if an umbrella company in the supply chain fails to pay correctly.

Conclusion:

Don’t rely on headline day rates. Plug your numbers into a reliable IR35 Calculator 2026/27 to compare inside vs outside scenarios accurately. Optimise with expenses, pensions, and status evidence. For personalised advice, consult a specialist accountant. This guide is for information only — tax rules are complex and individual.